Tizen OS vs Google TV: Key Differences, Features, and Which Smart TV Platform to Choose

Tatev Malkhasyan

February 13, 2026

19

minutes read

In this Tizen OS vs Google TV comparison, we break down how these two smart TV platforms differ and what that means for your media plan. The smart TV OS controls discovery, premium home-screen surfaces, and the data pathways behind CTV targeting and measurement — translating directly into practical implications for inventory access, audience strategy, and performance validation.

The “living room screen” isn’t just a TV anymore. For many households, it’s the entry point to streaming, a recommendation surface that shapes what gets watched next, and an ad environment where high-impact placements can sit directly on the home screen. That’s why Tizen OS vs Google TV has become more than a consumer comparison. For marketers, it’s a distribution decision that influences what viewers see first, which services get surfaced, and where premium inventory lives.

In this article, we’ll break down what Tizen OS and Google TV actually are, how each platform has evolved, and why their differences matter beyond the UI. We’ll compare them feature by feature, then zoom in on the areas that matter most to media teams: advertising and monetization capabilities, what inventory and data paths each OS tends to enable, and the practical implications for targeting and measurement.

⚡ The home screen isn’t a neutral menu; it’s a curated storefront. If you’re buying CTV without understanding the OS surfaces, you’re often ignoring the first impression.

What is Tizen OS?

Tizen OS is Samsung’s smart TV platform, used as the default operating system across Samsung smart TVs and positioned by Samsung as the software layer behind its Smart Hub experience (home screen, apps, and services). It runs the TV UI, supports the app framework and settings layer, and powers many of the “native” surfaces where content is discovered and promoted—including premium entry points that can also be monetized through Samsung’s ad products and owned services.

Tizen operating system background and evolution

Tizen began as an open-source operating system based on Linux, developed under open-source governance and hosted by the Linux Foundation. From the start, it was designed for “mobile and connected devices,” not just TVs, which is why it shows up historically across different device categories.

Over time, Samsung made Tizen central to its smart TV strategy, using it to control the end-to-end TV experience—how the home screen is organized, how content is surfaced, how apps are accessed, and how Samsung services integrate into everyday viewing. You can see that positioning in Samsung’s own Smart Hub/One UI Tizen materials, which frame Tizen as the backbone for its modern TV experience.

A practical way to think about Tizen today: it’s less “an OS in general” and more Samsung’s smart TV operating system layer—the software environment that defines discovery, navigation, and the on-TV surfaces Samsung can iterate on over time.

Key features of Tizen OS

At a platform level, Tizen’s differentiators tend to fall into three buckets.

Samsung-first navigation and services

Tizen is built around Samsung’s Smart Hub-style experience: quick access to apps, inputs, and entertainment services through a Samsung-controlled home screen. Samsung also positions its newer TV interface as One UI Tizen, which matters because it signals a more unified, consistent experience across TV model years (and gives Samsung a clearer “platform story” for ongoing updates).

SmartThings and device ecosystem integration

Tizen is closely tied to Samsung’s smart home ecosystem. Samsung explicitly calls out SmartThings connectivity within the One UI Tizen experience, which affects how device controls and connected-home experiences appear inside the TV interface.

Support and longevity signals

Samsung has made a notable support promise: “up to 7 years” of Tizen OS upgrades for One UI Tizen on eligible models. Reporting around the announcement indicates this policy starts with 2024 models and includes select 2023 TVs, which is unusually long in the TV category and can translate into more stable feature availability over time.

Supported devices and manufacturers

Historically, Samsung TVs were the primary home for Tizen, and that remains the center of gravity. What’s changing is Samsung’s push to broaden distribution through its Tizen OS licensing program, which allows other brands to ship TVs running Tizen in specific markets.

In a July 2025 update, Samsung said Tizen OS would be embedded in new TVs from partner brands across Europe, North America, Latin America, and Australia, and explicitly listed examples such as RCA in the United States and Canada (plus other regional brands).

For marketers, that matters because it hints at a future where “Tizen reach” is not perfectly synonymous with “Samsung TV reach.” It’s still Samsung-led, but the addressable footprint may broaden as licensing expands.

What is Google TV?

Google TV is Google’s content-first TV experience that comes built into certain smart TVs and streaming devices—and it runs on top of Android TV OS. In Google’s own words, Google TV is the “new, personalised experience,” while Android TV OS is the underlying operating system powering it.

In practice, Google TV is the layer that organizes apps and content into a unified “what to watch” interface: cross-app recommendations, curated collections, and a watchlist that follows you when you’re signed into your Google account.

It also functions as a distribution layer for Google. It’s where Google can integrate YouTube content, add new discovery modules (like a sports hub), and introduce advertiser-facing inventory on the TV screen, all while working within policy and consent requirements.

Google TV vs Android TV: what’s the difference?

The cleanest distinction is:

Android TV OS: the underlying operating system that powers TVs and streaming devices.

Google TV: the interface/experience layer that sits on top of Android TV OS and focuses on unified discovery and personalization.

Google spells this out directly: Google TV is powered by Android TV OS, and some devices may run Android TV OS without using the Google TV interface.

So when people compare “Google TV vs Android TV,” they’re usually comparing UI philosophy and discovery approach, not two entirely separate operating systems.

Key features of Google TV

Google TV’s strengths map closely to Google’s broader strategy: help users find content faster, personalize discovery across services, and connect the TV experience to Google’s ecosystem.

Content discovery across apps

Google TV is designed to surface what to watch, not just which app to open. Google describes the experience as bringing together movies, shows, and live TV “from across your apps and subscriptions” and organizing them in one place.

Google account-based personalization

Google TV’s personalization is closely tied to being signed in. For example, Google’s Google TV FAQ explicitly notes that some features (like watchlist access/editing) require a Google account sign-in.

That account link is one reason Google TV can support continuity across devices (watchlists, preferences, profiles), although the exact experience can vary by device and region.

Deep Google ecosystem integration (including YouTube and ads)

YouTube is deeply integrated into Google TV’s discovery model (Google’s product announcements routinely position YouTube highlights and YouTube content as part of the viewing experience).

On the advertising side, Google Ads describes the Google TV network as a way to extend YouTube video campaigns to in-feed and Masthead video inventory on the TV screen (and it lists supported countries, including the US).

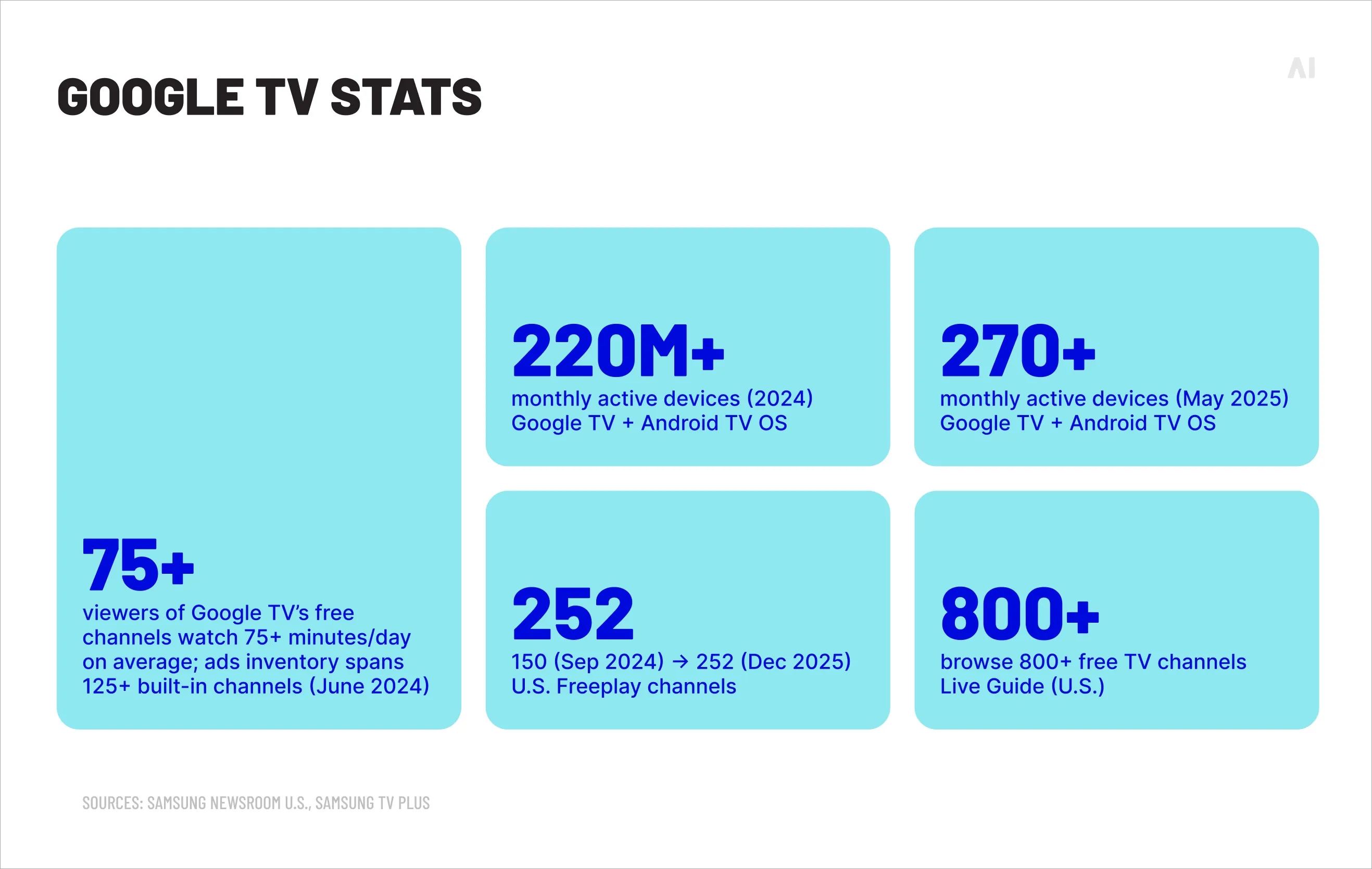

Google reported it is “bringing better TV to 270 million monthly active Google TV and other Android TV OS devices,” underscoring how broadly Android TV OS/Google TV spans OEMs and markets.

Supported brands and devices

Google TV appears on:

Smart TVs from multiple OEMs, with Google explicitly calling out device availability expanding across partners. In its September 2024 update, Google highlighted new Google TV devices including TVs from Hisense and TCL (plus other device categories like smart projectors).

Streaming devices, including Google’s own Google TV Streamer and other Google TV-enabled hardware.

Because Google TV is deployed across many manufacturers and hardware tiers, the “same” Google TV interface can feel different depending on chipset, memory, storage, and how consistently an OEM ships firmware updates. That variability is a real-world distinction versus Samsung’s more vertically integrated approach with Tizen.

Tizen OS vs Google TV: Feature-by-feature comparison

Here’s the core of Samsung Tizen vs Google TV for marketers: both ecosystems deliver streaming, app access, and personalization, but they organize attention differently (what gets surfaced first) and they connect to advertising stacks in different ways.

Quick comparison table: difference between Android and Tizen

Here’s a quick comparison table before we get into details:

{{26-Tizen-OS-vs-Google-TV-SEO-1="/tables"}}

User interface and navigation

Tizen UI tends to feel “device-native” because Samsung controls the whole stack. Samsung can design UI updates around its own remotes, menus, and service integrations, and deploy them across its product line.

Google TV’s UI is designed around discovery first. The home experience emphasizes what to watch and tries to reduce app switching. For marketers, that approach is important because the interface can influence where users spend time (and which services benefit from discovery placements).

A practical buying takeaway:

If your strategy relies on premium, native smart TV surfaces (like home screen modules), Samsung’s ecosystem is often straightforward because it’s centralized under Samsung’s TV experience.

If your strategy leans on Google’s distribution logic and identity, Google TV can be compelling because it connects to Google’s broader products.

⚡ If you can’t describe where the impression served—home screen, in-app, or FAST hub—CPM comparisons are often misleading. Placement context changes attention, completion behavior, and what “incremental” actually means.

Content discovery and recommendations

Discovery is where the “OS war” becomes real. The winner is often the platform that can best answer: What should I watch next?

{{26-Tizen-OS-vs-Google-TV-SEO-2="/tables"}}

Google TV leans into a recommendation engine built from Google’s understanding of content metadata and user preferences. Google also frames Google TV as a unified way to browse across services and interests.

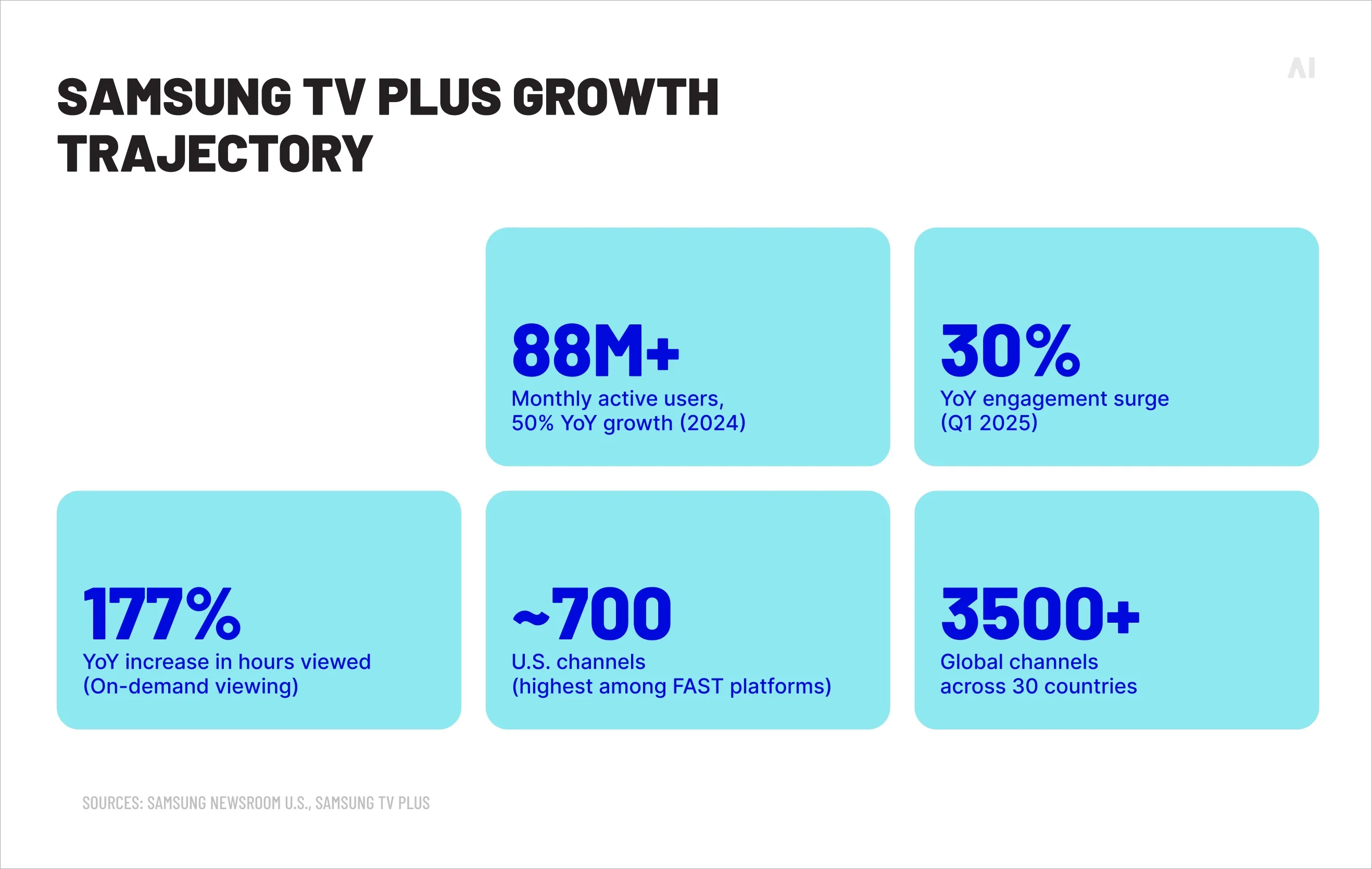

Samsung’s Tizen approach is typically more Samsung-service-forward (and can vary by model/year), but it still supports content hubs, featured rails, and FAST integration via Samsung TV Plus—an important driver of ad-supported viewing time for many households.

One nuance for advertisers: content discovery can influence attention quality. McKinsey notes that certain content types (sports/news, for example) can deliver meaningfully higher viewer focus than many other genres—so the OS’s ability to surface those genres (or steer to them) can have downstream effects on ad outcomes.

App ecosystem and streaming services

In 2026 planning, most brands assume the big apps exist everywhere. That’s mostly true. The differences that change media plans show up in:

Long-tail apps (niche sports networks, regional services, local news apps)

FAST channel depth and how tightly FAST is integrated into the OS

Regional availability and licensing differences

How aggressively the OS surfaces partner content

Google’s Android TV ecosystem is explicitly tied to the Google Play Store for Android TV, which supports a broad range of streaming apps, plus games. Samsung’s ecosystem sits inside Smart Hub and Samsung’s TV apps environment, and Samsung’s content and services may vary by region (a real consideration for international planning).

Voice assistants and smart home integration

Google TV naturally connects into Google’s voice and smart home layer. Android TV’s own product page states that Android TV “now comes with your Google Assistant built in,” including TV control and smart home actions like dimming lights.

Tizen aligns with Samsung’s SmartThings ecosystem. Samsung’s Tizen/Smart TV also features a built-in IoT hub concept, where Samsung Smart TVs can connect SmartThings-compatible devices to support a customized smart home experience.

For advertisers, the voice/smart home angle matters less for “voice search” and more for identity continuity and household graphs. Signed-in ecosystems can create stronger continuity across devices; device-centric ecosystems can create strong household-level signals through TV usage patterns.

Performance and system speed

Performance is a “quiet” factor that still matters. If a TV OS is sluggish, viewers usually do one of three things:

Spend less time browsing and more time launching the same apps

Switch to external devices (Roku/Fire TV/Apple TV/consoles)

Disengage faster

Tizen performance tends to be more predictable within Samsung’s lineup because Samsung controls both OS experience and TV product strategy. Google TV performance varies more because Google TV ships across many partner brands and device tiers. Google TV also comes built-in to devices from “top brands,” which is great for scale but naturally introduces hardware and update variability.

From a media perspective, performance affects:

Session depth (how long users browse and discover)

App switching (which can change attribution paths)

Likelihood of staying on OS-native surfaces (where OEM ad inventory often lives)

Most buyers don’t lose sleep over whether Netflix is available. They lose sleep over the edge cases that can quietly impact reach and delivery: a regional streamer that isn’t supported in one market, a FAST experience that behaves differently on the home screen, or a niche category where one ecosystem simply has more viable apps.

Streaming apps and media platforms

Here’s the practical checklist for Google TV vs Samsung TV app planning:

Are the “must-have” streamers present in your target region?

Are local broadcasters or regional streamers present?

Is FAST integrated at the OS level or treated as “just another app”?

How does the OS promote certain services on the home screen?

⚡ Most delivery issues don’t come from missing major apps—they come from regional and niche gaps you didn’t QA. Treat app availability like a targeting constraint, not a technical footnote.

{{26-Tizen-OS-vs-Google-TV-SEO-3="/tables"}}

Google TV’s cross-app discovery tends to help content get surfaced through aggregated rails. Samsung’s environment can be powerful when Samsung services (like Samsung TV Plus) are deeply integrated into default experiences.

Google TV / Android TV often has stronger coverage for niche categories because developers can more easily target Android TV distribution and reuse Android tooling.

Tizen can be strong in Samsung-led experiences and partnerships, but the long-tail can vary by region and device year.

For marketers, niche apps matter when your audience lives in them: fitness subscriptions, kids content platforms, niche sports streaming, or international programming hubs. Even small differences in app availability can shift your reachable universe in meaningful ways, especially once you start layering frequency controls and brand-safety adjacency rules.

App update frequency and long-term support

Two separate questions get conflated here:

Does the OS itself get updated? Samsung’s “seven years of Tizen OS updates” signal is notable because it implies longer platform consistency for supported models.

Do apps get updated consistently? App updates depend on developer priorities and store pipelines. Google TV benefits from Android ecosystem tooling, while Samsung relies on its store environment and partnerships.

Planning tip: if you’re building a multi-year CTV roadmap, ask OEM/platform partners about:

Typical OS update cadence by model year

App update approval timelines

How deprecated models are handled (especially for ad formats that require newer firmware)

Advertising and monetization capabilities

If you’re reading this as a buyer, this section is the point. Because “best smart TV OS” often means best monetization surfaces + best data path + easiest buying workflow.

{{26-Tizen-OS-vs-Google-TV-SEO-4="/tables"}}

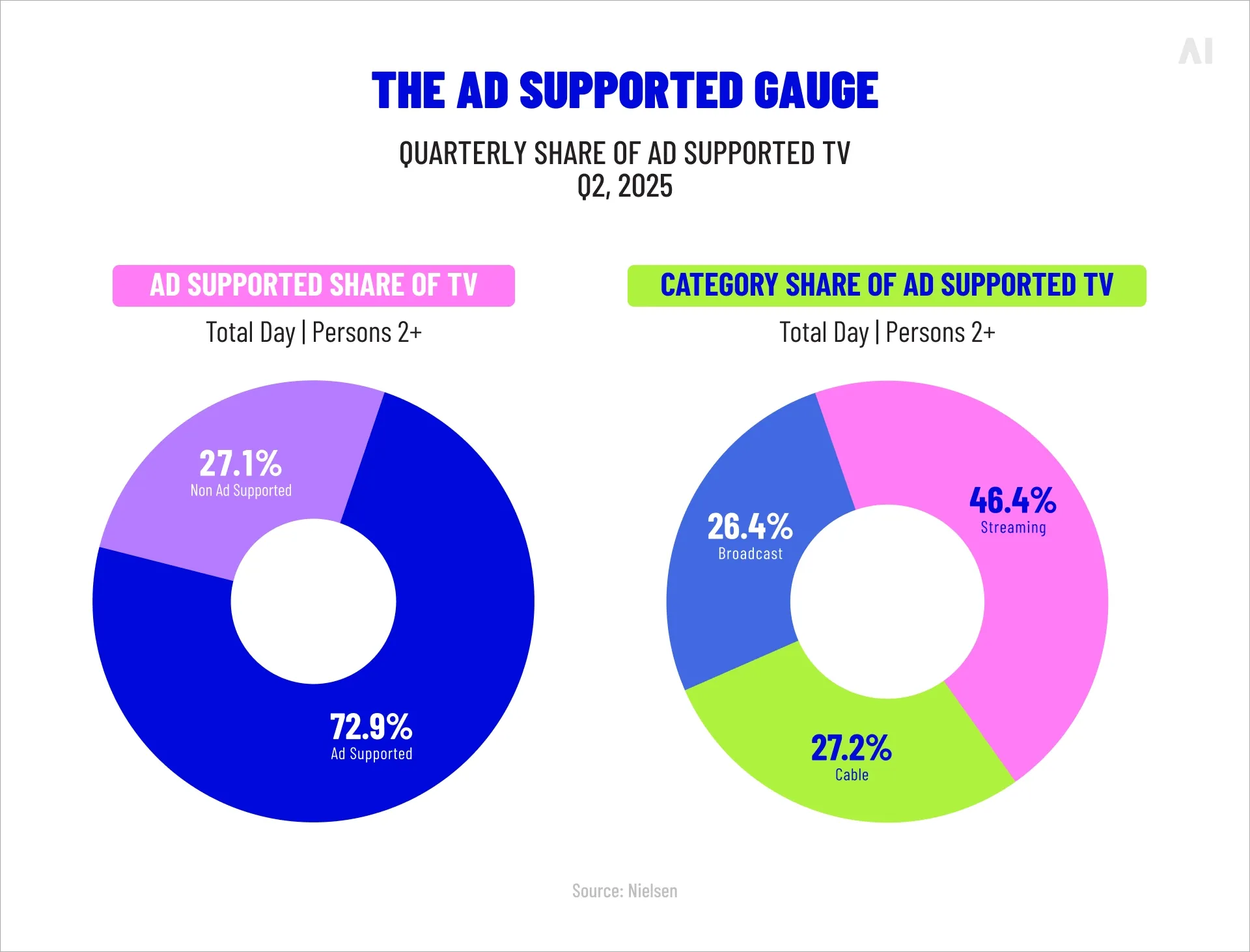

Nielsen: Ad-supported share of TV (Q3 2025) (Source}

Ads on Google TV: data, targeting, and Google ecosystem

Google TV inventory can be accessed through Google’s advertising products in specific ways. Google Ads describes the Google TV network and the ability to run eligible formats (such as in-feed ads for certain Video Reach Campaign setups), with support for audience segment and location targeting.

Google also provides a dedicated Google TV Masthead format (a prominent, high-visibility placement).

⚡ Google TV Masthead is designed to be the first thing viewers see before organic recommendations. That makes it a strong “launch moment” format, but only if the rest of your plan can capture and validate the downstream lift.

From a media ops perspective, Google TV’s advantages usually come from:

Familiar workflows (Google Ads / Google Marketing Platform environments)

Audience logic tied to Google identity and intent signals (where applicable)

Easier alignment with YouTube and broader Google video strategies

Where buyers should be careful:

Inventory definitions (what exactly counts as Google TV network inventory vs YouTube vs other CTV placements)

Reporting clarity (placement transparency, device/environment breakdowns, and how measurement is modeled)

Samsung’s ad story is tightly connected to Samsung’s TV footprint and Samsung-owned/operated surfaces.

Two scale points buyers often reference:

Samsung TV Plus reported88 million monthly active users (global) in 2025, and described strong growth in viewership.

Samsung Ads messaging highlights a large Samsung Smart TV footprint in the US (useful for reach planning and ACR-based segments), though exact numbers can vary depending on the measurement definition used in a given report.

Samsung also markets home screen ad products such as sponsored tiles within Smart Hub experiences.

For advertisers, the Samsung value proposition is often:

OEM-native inventory (home screen placements, Samsung TV Plus environments)

Automatic Content Recognition (ACR)-style signals used for segments and measurement (with opt-outs and regional privacy differences)

A walled-garden-like feel, but on the device level rather than the app level

A useful illustration (not a universal benchmark): AdExchanger published a Samsung Ads case study describing strong brand lift outcomes for a campaign using Samsung Ads data and placements. Treat these as directional examples, not guarantees.

What advertisers should know about each platform

If you want the short version:

Choose Google TV when you want Google-native audience workflows, alignment with YouTube, and broad Android TV scale.

Choose Tizen / Samsung when you want Samsung-native surfaces and a clearer OEM-led footprint, especially when Samsung TV Plus and home screen inventory matter to your strategy.

But most real plans shouldn’t choose one. They should plan for both and define what each ecosystem is “for.”

A practical framework for media buyers:

Use Google TV for scale and Google-aligned audience strategies.

Use Samsung/Tizen for OEM-native reach, home screen visibility, and Samsung-owned environments.

Normalize measurement with a clear incrementality approach (holdouts, lift tests, or matched-market where feasible).

Nielsen’s 2025 analysis of streaming emphasizes the dominance of ad-supported viewing within streaming time—another reason OS-level discovery and ad surfaces matter.

Both platforms personalize experiences and ads, but they do it through different identity and data approaches and that changes the consent conversation.

User data collection and privacy controls

Before getting into platform specifics, it helps to separate two questions that often get blurred together: what data the TV OS can collect and what the user can realistically control. Smart TV privacy isn’t just a policy page. It’s a mix of device settings (often buried), account-level preferences, and region-specific defaults that can change what signals are available for personalization, targeting, and measurement. For advertisers, the practical takeaway is simple: the same campaign can behave differently depending on whether households are signed in, whether ad personalization is enabled, and whether TV-level viewing recognition features are on or off—so it’s worth understanding these controls before you interpret reach, frequency, or performance data:

Google TV: Google provides ad controls through tools like My Ad Center and ad personalization settings, allowing users to adjust or turn off personalized ads in supported contexts. Google also documents the Google TV network’s ad mechanics in its help materials (useful for understanding targeting and eligibility).

Tizen / Samsung TVs: Smart TV data collection often includes device usage data and, in many cases, ACR-based viewing recognition depending on settings and region. Consumer Reports has published practical guidance on disabling “smart TV snooping” style features on major brands, reflecting how real households experience these controls.

{{26-Tizen-OS-vs-Google-TV-SEO-5="/tables"}}

There’s also increasing regulatory and legal scrutiny of smart TV tracking. For example, The Verge reported on Texas lawsuits alleging improper smart TV surveillance via ACR-style tracking across multiple TV manufacturers. (This is not a verdict on any specific platform’s compliance; it’s a reminder that the privacy environment is tightening.)

From a marketer viewpoint, personalization impacts two things:

Content adjacency: If an OS pushes a viewer toward a genre (sports, reality, kids), your campaigns inherit those adjacency patterns.

Audience shaping: Recommendation loops can change what a household watches over time, which can change behavioral segments (again, depending on consent and data use policies).

Google TV’s personalization often leans on Google account signals when users are signed in. Tizen’s personalization tends to be more Samsung ecosystem-driven and can be influenced by Samsung services and device settings.

If you buy CTV at scale, assume this will be a bigger deal in 2026+.

Your best practices checklist:

Ask for “what data is used” in plain language, not just “privacy-safe.” (You want to know whether it’s account-based, device-based, ACR-influenced, contextual, or modeled.)

Understand opt-out behavior and its impact. For Google, that means knowing how ad personalization controls affect ad experiences on connected TV devices. For smart TVs broadly, it means knowing what happens when ACR-style features are turned off.

Design measurement that survives signal loss: incrementality tests, modeled conversions, and MMM support where appropriate.

Document consent assumptions in your internal measurement notes so stakeholders don’t overinterpret precision, especially when different platforms are using different signal types under the hood.

⚡ Assume opt-outs will happen and build your measurement to survive them. The strongest teams treat deterministic targeting as a bonus and incrementality as the baseline.

Regional availability and market share

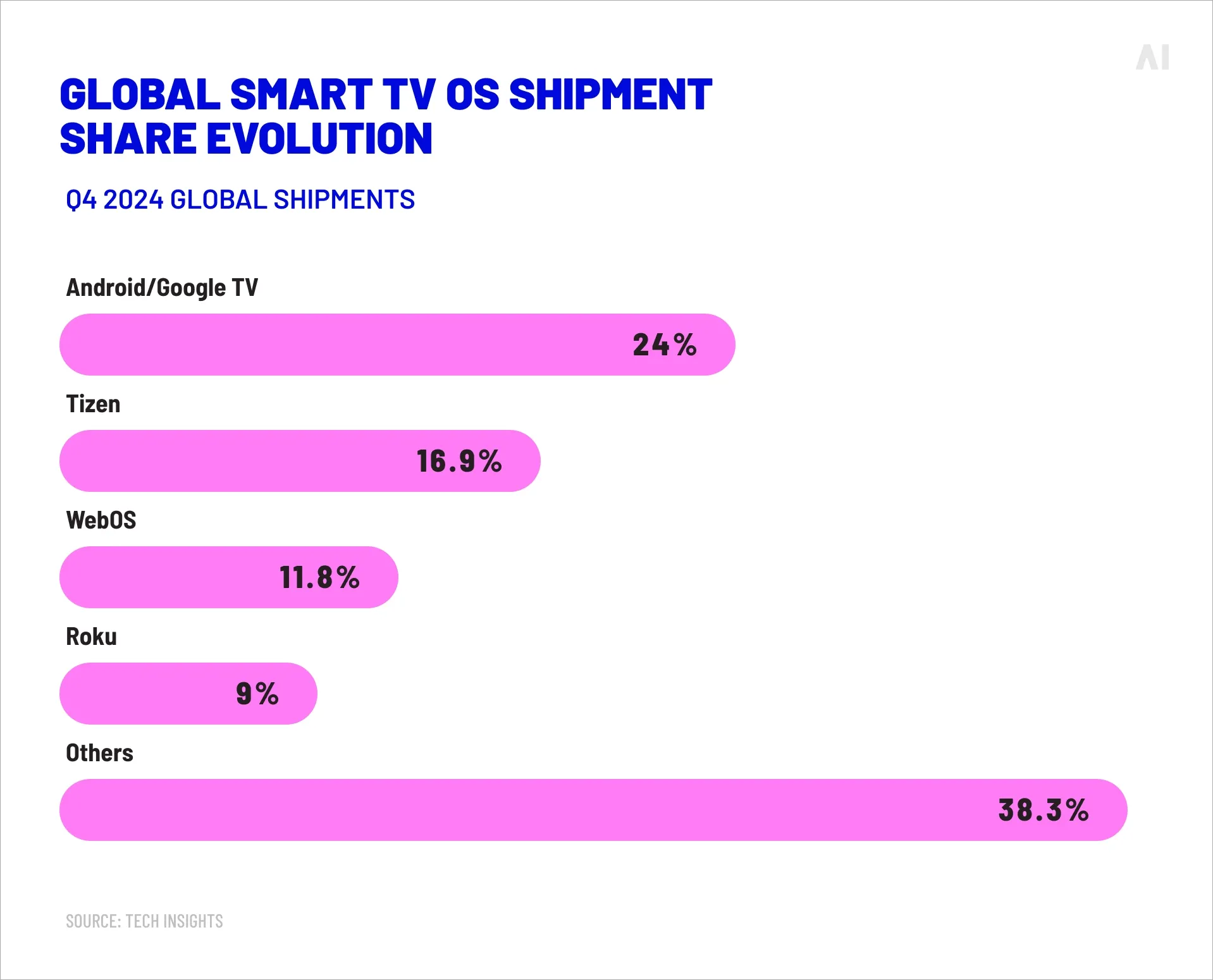

Smart TV OS share is not uniform worldwide. Even when two platforms are global, their dominance is regional—and it also depends on which metric you’re looking at (shipments vs installed base vs programmatic ad delivery). Shipment share is useful for forecasting future footprints, but buyers should sanity-check it against where their impressions actually clear in-market. TechInsights, for example, frames its Q4 2024 OS analysis explicitly around global shipments and regional breakdowns, covering six regions (and, in a related cut, dozens of countries).

Global smart TV OS shipment share evolution (Source)

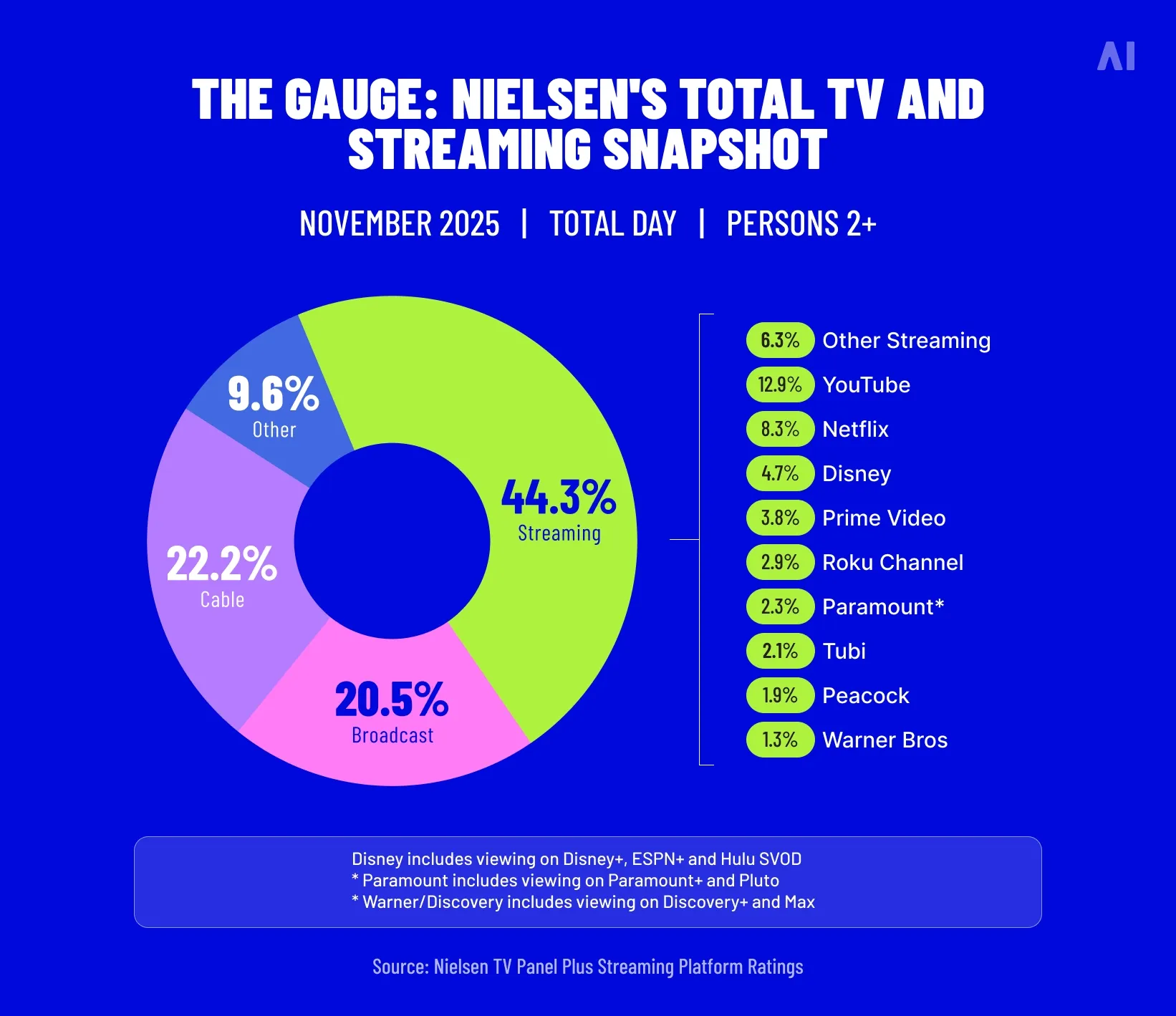

⚡Streaming has become the default TV behavior in the U.S., which amplifies the importance of OS-level discovery. Nielsen reported streaming reached 46.7% of total TV viewing in November 2025—an attention shift that makes home screen real estate more valuable to advertise.

Tizen’s advantage starts with Samsung’s TV footprint and gets reinforced by Samsung’s push to extend Tizen beyond Samsung-branded sets.

Global shipment presence: TechInsights estimates that in Q4 2024, Android/Google TV accounted for over 24% of global smart TV shipments, ahead of Tizen at 16.9% (with webOS at 11.8% and Roku at 9%). That ~17% shipment share is a big reason Tizen remains a top-tier OS for marketers planning global or multi-market CTV programs: it represents a large, continuing pipeline of devices entering households.

Licensing expansion signal: As mentioned, Samsung’s July 2025 announcement expanded its Tizen OS Licensing Program and explicitly said Tizen will be embedded in new TVs from partner brands across Europe, North America, Latin America, and Australia, naming examples like RCA (Treasure Creek) in the U.S. and Canada and RCA (Kayve Groupo) in Mexico—with “many more brands” expected to join in 2H 2025. For planners, this is the key nuance: “Tizen reach” may start to become larger than Samsung-only reach in some markets over time. It’s still Samsung-led, but the footprint can broaden.

⚡ Samsung’s scale isn’t abstract; it shows up in household penetration. Parks Associates reported that 68% of U.S. internet households owned a smart TV in late 2024, and Samsung was the most-used brand in 37% of connected TV homes—useful context when you’re modeling OEM-native reach.

Google TV’s growth story is multi-OEM by design, and Google has been explicit about both its scale and its market expansion.

Scale across devices: Google reported it is now bringing Google TV to 270 million monthly active Google TV and other Android TV OS devices (as of September 2024).

Country expansion: In the same update, Google noted that Google TV is expanding to more countries including Thailand, Indonesia, Vietnam, and the Philippines—a useful reminder that some of the fastest unit growth can come from markets where smart TV adoption is accelerating and OEM diversity is high.

One practical reason Google TV/Android TV-based devices can scale quickly in high-growth segments: many manufacturers can adopt an existing platform rather than building and maintaining a TV OS from scratch, which tends to increase the number of brands and price tiers shipping the platform.

Implications for users and advertisers

For advertisers, regional OS realities translate into planning realities:

In some markets, Samsung/Tizen will be your most direct route to OEM-native reach (especially if you care about home-screen and OEM-controlled placements).

In others, Google TV/Android TV will deliver broader device coverage across multiple brands, which can matter when you’re optimizing for reach at efficient CPMs.

Your best plan often uses both, then normalizes measurement across environments (lift, holdouts, matched-market) so stakeholders don’t mistake platform-level reporting differences for true performance differences.

One extra US-specific caution: global smart TV shipment share doesn’t always mirror US programmatic delivery reality. A Pixalate-based analysis cited by TVTechnology found Roku and Amazon leading US connected TV device share by programmatic ad delivery in Q2 2025, with Samsung in the next tier (alongside Apple) at around 12%. That doesn’t replace OS share analysis, but it’s a useful “reality check” for where impressions may actually clear in the US.

This is the scannable “Tizen TV vs Google TV” view.

Pros and cons of Tizen OS

Tizen’s trade-offs are shaped by one core reality: Samsung owns the full TV stack. That typically delivers a more uniform experience across Samsung sets and gives Samsung clear control over home screen surfaces and service integrations. The flipside is that ecosystem breadth, especially in niche and regional app availability, can be less predictable than in a platform built to span many manufacturers.

Pros

Samsung-led consistency across UX and many model years

Strong integration with Samsung services (including Samsung TV Plus)

Growing licensing footprint could expand reach beyond Samsung-only sets

Longer OS support promise for newer models (seven years for specified TVs)

Cons

App ecosystem can be less flexible in long-tail categories versus Android-based platforms

More “Samsung-shaped” environment: great if you want it, limiting if you need broad cross-OEM uniformity

Privacy expectations and ACR scrutiny are rising across smart TV ecosystems

Pros and cons of Google TV

Google TV’s trade-offs come from the opposite model: it’s designed to scale across many OEMs and device tiers, with discovery and personalization anchored in Google’s content and account ecosystem. That can be a major advantage for cross-device audience strategies, but it also introduces more variability in hardware performance, update cadence, and what “Google TV inventory” means in a given buying setup.

Large multi-OEM scale (270M monthly active Android TV OS/Google TV devices)

Easier alignment with Google buying and identity ecosystems (where applicable)

Cons

Performance and UX consistency vary by OEM hardware and update policy

Inventory definitions can be confusing (Google TV network vs YouTube vs other CTV)

As with any signed-in ecosystem, personalization and privacy controls must be clearly understood

Which platform should you choose?

This depends on who you are: ecosystem user, buyer, or advertiser.

Best for Samsung ecosystem users

Pick Tizen (Samsung TVs) when:

You already use Samsung devices or SmartThings

You want a consistent Samsung experience across hardware

You value Samsung service integration (Samsung TV Plus, Samsung UI features)

Best for Google ecosystem users

Pick Google TV when:

You’re heavily Google-signed-in (YouTube, Google services, Google Home)

You prefer content-forward recommendations and unified watchlists

You want broad OEM choice across price tiers

Best for advertisers and brands

If you’re choosing for advertising (not personal use), use this decision tree:

Do you need Google-native workflows and YouTube alignment? Start with Google TV/Android TV placements where they fit your targeting and reporting needs.

Do you need OEM-native home screen visibility and Samsung-owned surfaces? Layer in Samsung Ads/Tizen inventory, especially if Samsung TV Plus and Smart Hub placements matter.

Do you need a privacy-resilient measurement plan? Build incrementality into your plan from day one. Don’t rely only on deterministic identity.

A few trends are likely to shape the next phase of Google TV vs Tizen for advertisers, but the headline is simple: smart TV operating systems are starting to behave less like “menus” and more like media layers that control discovery, premium placements, and the data path that sits behind CTV delivery and measurement.

More premium home screen ad real estate: OEMs and platforms are treating the TV home screen like a monetizable surface, not a neutral menu. Expect more sponsored modules, more commerce experiments, and more retail-media-like logic applied to TV discovery.

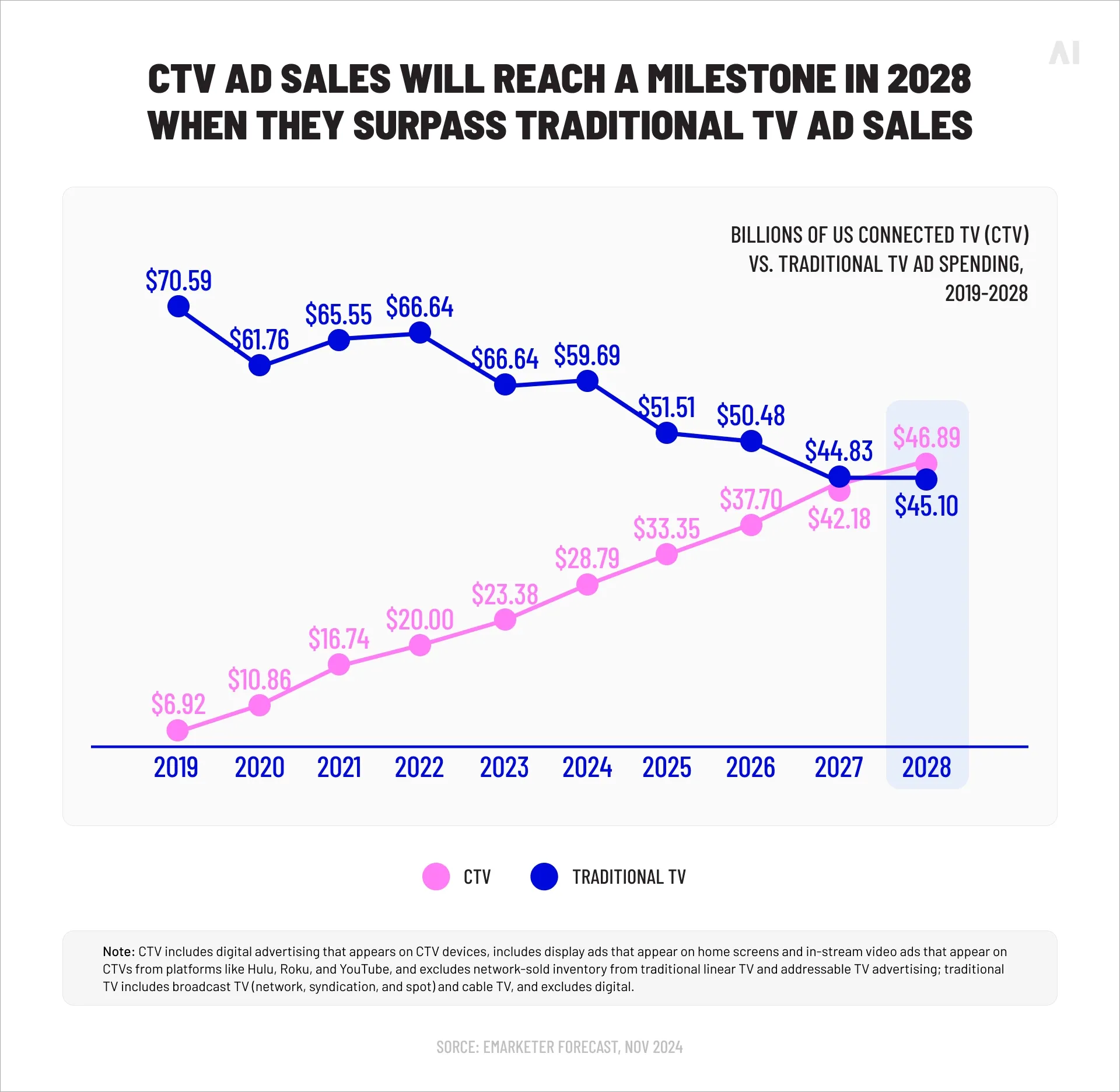

CTV spend keeps rising, so platform differentiation matters more: PwC’s Global Entertainment & Media outlook projects global connected TV advertising revenue climbing substantially in the coming years (reaching $51B in 2029). As money follows attention, OS ecosystems will keep competing for control of discovery and inventory.

AI-driven discovery becomes more aggressive: “Recommendation engines” are likely to become more proactive: summarizing shows, surfacing clips, building collections, and driving viewers into ad-supported content environments.

Longer OS support windows become part of the buying pitch: Samsung’s seven-year OS update promise hints at a future where TV OS support becomes a selling point like smartphone updates.

Conclusion: choosing between two powerful Smart TV ecosystems

The real answer to Tizen OS vs Google TV is not “one is better.” It’s that each platform represents a different kind of advantage:

Tizen is strongest when you want a Samsung-led, OEM-native environment—with Samsung-controlled home screen surfaces, Samsung services (including Samsung TV Plus), and a licensing push that could expand Tizen’s footprint beyond Samsung-only sets over time.

Google TV is strongest when you want content-first discovery layered onto Android TV scale, with clearer ties to Google account-based experiences and Google buying surfaces like the Google TV network and Masthead placements.

For marketers, the best move is rarely picking a single OS. It’s building an approach that treats smart TV operating systems as distribution layers, then aligning inventory access, targeting logic, and measurement to what each ecosystem does best.

Where AI Digital can help you turn this into a plan

If you’re trying to operationalize “plan for both” (without duplicating waste or getting trapped in platform bias), AI Digital can help you map the smart TV OS layer into a clean CTV execution strategy. AI Digital’s model is DSP-agnostic, client-first, and built for transparency across fragmented channels, using its Open Garden framework and managed service approach.

A practical next step for many brands is tightening the supply path and controlling where CTV spend actually clears. That’s where Smart Supply comes in.

Smart Supply is AI Digital’s supply-side solution, designed to help brands execute optimized supply strategies across Streaming Video and CTV, not just display.

It’s built to reduce inventory bias (for example, when platforms prioritize their own owned-and-operated inventory), keeping prioritization tied to performance against your KPIs.

Deals are custom-built and continuously optimized, with a curation funnel that filters out low-performing publishers, reduces unnecessary bid hops, and applies IVT protection—so buyers can focus on quality, direct supply.

It’s a tool, not a media vendor—DSP-agnostic, with rapid activation (deal IDs issued within 24 hours), and structured to minimize added friction in execution.

If you want help designing a CTV plan that accounts for both Tizen and Google TV (inventory, targeting, and measurement), get in touch with AI Digital and ask about Smart Supply (AI Digital service page).

Blind spot

Key issues

Business impact

AI Digital solution

Lack of transparency in AI models

• Platforms own AI models and train on proprietary data • Brands have little visibility into decision-making • "Walled gardens" restrict data access

• Inefficient ad spend • Limited strategic control • Eroded consumer trust • Potential budget mismanagement

Open Garden framework providing: • Complete transparency • DSP-agnostic execution • Cross-platform data & insights

Optimizing ads vs. optimizing impact

• AI excels at short-term metrics but may struggle with brand building • Consumers can detect AI-generated content • Efficiency might come at cost of authenticity

• Short-term gains at expense of brand health • Potential loss of authentic connection • Reduced effectiveness in storytelling

Smart Supply offering: • Human oversight of AI recommendations • Custom KPI alignment beyond clicks • Brand-safe inventory verification

The illusion of personalization

• Segment optimization rebranded as personalization • First-party data infrastructure challenges • Personalization vs. surveillance concerns

• Potential mismatch between promise and reality • Privacy concerns affecting consumer trust • Cost barriers for smaller businesses

Elevate platform features: • Real-time AI + human intelligence • First-party data activation • Ethical personalization strategies

AI-Driven efficiency vs. decision-making

• AI shifting from tool to decision-maker • Black box optimization like Google Performance Max • Human oversight limitations

• Strategic control loss • Difficulty questioning AI outputs • Inability to measure granular impact • Potential brand damage from mistakes

Managed Service with: • Human strategists overseeing AI • Custom KPI optimization • Complete campaign transparency

Fig. 1. Summary of AI blind spots in advertising

Dimension

Walled garden advantage

Walled garden limitation

Strategic impact

Audience access

Massive, engaged user bases

Limited visibility beyond platform

Reach without understanding

Data control

Sophisticated targeting tools

Data remains siloed within platform

Fragmented customer view

Measurement

Detailed in-platform metrics

Inconsistent cross-platform standards

Difficult performance comparison

Intelligence

Platform-specific insights

Limited data portability

Restricted strategic learning

Optimization

Powerful automated tools

Black-box algorithms

Reduced marketer control

Fig. 2. Strategic trade-offs in walled garden advertising.

Core issue

Platform priority

Walled garden limitation

Real-world example

Attribution opacity

Claiming maximum credit for conversions

Limited visibility into true conversion paths

Meta and TikTok's conflicting attribution models after iOS privacy updates

Data restrictions

Maintaining proprietary data control

Inability to combine platform data with other sources

Amazon DSP's limitations on detailed performance data exports

Cross-channel blindspots

Keeping advertisers within ecosystem

Fragmented view of customer journey

YouTube/DV360 campaigns lacking integration with non-Google platforms

Black box algorithms

Optimizing for platform revenue

Reduced control over campaign execution

Self-serve platforms using opaque ML models with little advertiser input

Performance reporting

Presenting platform in best light

Discrepancies between platform-reported and independently measured results

Consistently higher performance metrics in platform reports vs. third-party measurement

Fig. 1. The Walled garden misalignment: Platform interests vs. advertiser needs.

Key dimension

Challenge

Strategic imperative

ROAS volatility

Softer returns across digital channels

Shift from soft KPIs to measurable revenue impact

Media planning

Static plans no longer effective

Develop agile, modular approaches adaptable to changing conditions

Brand/performance

Traditional division dissolving

Create full-funnel strategies balancing long-term equity with short-term conversion

Capability

Key features

Benefits

Performance data

Elevate forecasting tool

• Vertical-specific insights • Historical data from past economic turbulence • "Cascade planning" functionality • Real-time adaptation

• Provides agility to adjust campaign strategy based on performance • Shows which media channels work best to drive efficient and effective performance • Confident budget reallocation • Reduces reaction time to market shifts

• Dataset from 10,000+ campaigns • Cuts response time from weeks to minutes

• Reaches people most likely to buy • Avoids wasted impressions and budgets on poor-performing placements • Context-aligned messaging

• 25+ billion bid requests analyzed daily • 18% improvement in working media efficiency • 26% increase in engagement during recessions

Full-funnel accountability

• Links awareness campaigns to lower funnel outcomes • Tests if ads actually drive new business • Measures brand perception changes • "Ask Elevate" AI Chat Assistant

• Upper-funnel to outcome connection • Sentiment shift tracking • Personalized messaging • Helps balance immediate sales vs. long-term brand building

• Natural language data queries • True business impact measurement

Open Garden approach

• Cross-platform and channel planning • Not locked into specific platforms • Unified cross-platform reach • Shows exactly where money is spent

• Reduces complexity across channels • Performance-based ad placement • Rapid budget reallocation • Eliminates platform-specific commitments and provides platform-based optimization and agility

• Coverage across all inventory sources • Provides full visibility into spending • Avoids the inability to pivot across platform as you’re not in a singular platform

Fig. 1. How AI Digital helps during economic uncertainty.

Trend

What it means for marketers

Supply & demand lines are blurring

Platforms from Google (P-Max) to Microsoft are merging optimization and inventory in one opaque box. Expect more bundled “best available” media where the algorithm, not the trader, decides channel and publisher mix.

Walled gardens get taller

Microsoft’s O&O set now spans Bing, Xbox, Outlook, Edge and LinkedIn, which just launched revenue-sharing video programs to lure creators and ad dollars. (Business Insider)

Retail & commerce media shape strategy

Microsoft’s Curate lets retailers and data owners package first-party segments, an echo of Amazon’s and Walmart’s approaches. Agencies must master seller-defined audiences as well as buyer-side tactics.

AI oversight becomes critical

Closed AI bidding means fewer levers for traders. Independent verification, incrementality testing and commercial guardrails rise in importance.

Fig. 1. Platform trends and their implications.

Metric

Connected TV (CTV)

Linear TV

Video Completion Rate

94.5%

70%

Purchase Rate After Ad

23%

12%

Ad Attention Rate

57% (prefer CTV ads)

54.5%

Viewer Reach (U.S.)

85% of households

228 million viewers

Retail Media Trends 2025

Access Complete consumer behaviour analyses and competitor benchmarks.

Identify and categorize audience groups based on behaviors, preferences, and characteristics

Michaels Stores: Implemented a genAI platform that increased email personalization from 20% to 95%, leading to a 41% boost in SMS click through rates and a 25% increase in engagement.

Estée Lauder: Partnered with Google Cloud to leverage genAI technologies for real-time consumer feedback monitoring and analyzing consumer sentiment across various channels.

High

Medium

Automated ad campaigns

Automate ad creation, placement, and optimization across various platforms

Showmax: Partnered with AI firms toautomate ad creation and testing, reducing production time by 70% while streamlining their quality assurance process.

Headway: Employed AI tools for ad creation and optimization, boosting performance by 40% and reaching 3.3 billion impressions while incorporating AI-generated content in 20% of their paid campaigns.

High

High

Brand sentiment tracking

Monitor and analyze public opinion about a brand across multiple channels in real time

L’Oréal: Analyzed millions of online comments, images, and videos to identify potential product innovation opportunities, effectively tracking brand sentiment and consumer trends.

Kellogg Company: Used AI to scan trending recipes featuring cereal, leveraging this data to launch targeted social campaigns that capitalize on positive brand sentiment and culinary trends.

High

Low

Campaign strategy optimization

Analyze data to predict optimal campaign approaches, channels, and timing

DoorDash: Leveraged Google’s AI-powered Demand Gen tool, which boosted its conversion rate by 15 times and improved cost per action efficiency by 50% compared with previous campaigns.

Kitsch: Employed Meta’s Advantage+ shopping campaigns with AI-powered tools to optimize campaigns, identifying and delivering top-performing ads to high-value consumers.

High

High

Content strategy

Generate content ideas, predict performance, and optimize distribution strategies

JPMorgan Chase: Collaborated with Persado to develop LLMs for marketing copy, achieving up to 450% higher clickthrough rates compared with human-written ads in pilot tests.

Hotel Chocolat: Employed genAI for concept development and production of its Velvetiser TV ad, which earned the highest-ever System1 score for adomestic appliance commercial.

High

High

Personalization strategy development

Create tailored messaging and experiences for consumers at scale

Stitch Fix: Uses genAI to help stylists interpret customer feedback and provide product recommendations, effectively personalizing shopping experiences.

Instacart: Uses genAI to offer customers personalized recipes, mealplanning ideas, and shopping lists based on individual preferences and habits.

Medium

Medium

Share article

Url copied to clipboard

No items found.

Subscribe to our Newsletter

THANK YOU FOR YOUR SUBSCRIPTION

Oops! Something went wrong while submitting the form.

Questions? We have answers

What is Tizen smart TV?

A smart TV by Tizen is a Samsung-led smart television that runs the Tizen operating system, which controls the home screen, app experience, content discovery surfaces, and (in many cases) Samsung-native services like Samsung TV Plus and SmartThings integration.

What is the main difference between Tizen OS and Google TV?

Tizen OS is Samsung’s proprietary smart TV platform and UI layer, while Google TV is Google’s content-first interface that runs on top of Android TV OS across many TV brands and devices.

Which is better, Tizen or Google TV?

It depends on what you care about most. Tizen tends to be a strong fit if you want a consistent Samsung-led TV experience and tight integration with Samsung services, while Google TV is often better if you prefer cross-app discovery and a Google account-centric ecosystem across many device brands.

What are the disadvantages of Tizen TV?

The long-tail app ecosystem can be less flexible than Android-based platforms, availability can vary by region, and smart TV privacy expectations are rising—especially around device-level tracking like ACR, which some households disable.

Is Tizen a good OS for TV?

Yes. Samsung positions One UI Tizen as a unified smart TV experience, and the company has also stated that eligible models can receive up to seven years of One UI Tizen upgrades, which can support longer platform consistency.

Which smart TVs use Google TV?

Google TV appears on TVs from multiple manufacturers and on streaming devices; Google has highlighted availability across various partner brands and regions as the ecosystem expands.

Can you install the same apps on both platforms?

Many major streaming apps are available on both, but the overlap is not perfect, especially for regional services and niche categories, because Google TV relies on the Android TV/Google Play ecosystem while Samsung uses its Smart Hub app environment and availability can vary by region.

Have other questions?

If you have more questions, contact us so we can help.

.svg)

.svg)